Higher Wages Bring Credit Opportunities

There has been a lot of activity in the state legislature over the last six months that will impact central Illinois businesses. At the top of the list is the new law that raises the minimum wage. SB1, “Lifting Up Illinois Working Families Act,” was signed by Governor J.B. Pritzker in February and goes into effect on January 1, 2020. While the minimum wage increase was a hot topic in the media, the payroll withholding tax credit for small employers received less coverage—and it might help your business absorb the changes.

Background of SB1

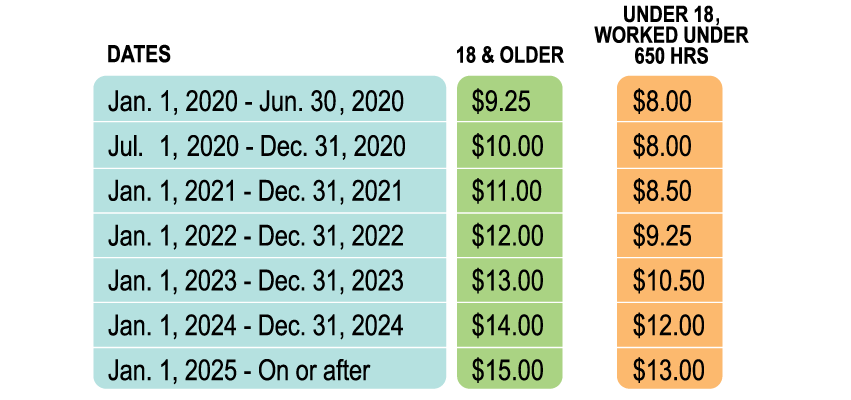

Prior to the new law, the $8.25 minimum wage in Illinois had remained the same for individuals ages 18 and older since 2010. SB1 phases in the increased minimum wage for these individuals at a rate of approximately $1 per year until 2025, when it reaches $15 per hour. A higher minimum wage will also go into effect for individuals under the age of 18 who worked under 650 hours for the employer per calendar year. Below is a summary of the minimum wage increases mandated by SB1:

How the Payroll Credit Works

As a summary, eligible employers may claim a payroll withholding tax credit for a percentage of the difference between qualified employees’ prior wages and increased wages under the new law. The credit can be claimed on quarterly Illinois income tax withholding returns filed for the period beginning January 1, 2020. The credit is not refundable and cannot exceed the employer’s tax liability for the reporting period.

Qualifying Rules

Employers with 50 or fewer Illinois full-time employees who make the minimum wage may qualify for the credit. The credit excludes employees who have worked fewer than 90 consecutive days before the reporting period. However, credits can accrue during that 90-day period for future reporting periods.

Not every small business will be eligible to claim this credit. In order to qualify, an employer’s average wage paid to each employee making less than $55,000 annually must have increased over the average wage paid in the prior year for employees making less than $55,000.

The credit is calculated as a percentage of the difference between wages paid in Illinois during the reporting period to employees who made minimum wage or less than minimum wage. The maximum credit allowed is as follows:

- 25% for 2020

- 21% for 2021

- 17% for 2022

- 13% for 2023

- 9% for 2024

- 5% for 2025

- 5% for 2026 (but only for employers with more than five employees)

- 5% for 2027 (only for employers with five or fewer employees)

While much has been written on both sides as to the pros and cons of this new legislation, the wage increase is coming regardless. So explore the credit opportunities and plan for the disruption with your tax advisors—it will help you absorb the changes so you can continue to propel your business forward. PM

The information contained herein is general in nature and is not intended, and should not be construed, as legal, accounting, investment or tax advice or opinion provided by CliftonLarsonAllen LLP (CliftonLarsonAllen) to the reader. For more information, visit CLAconnect.com.